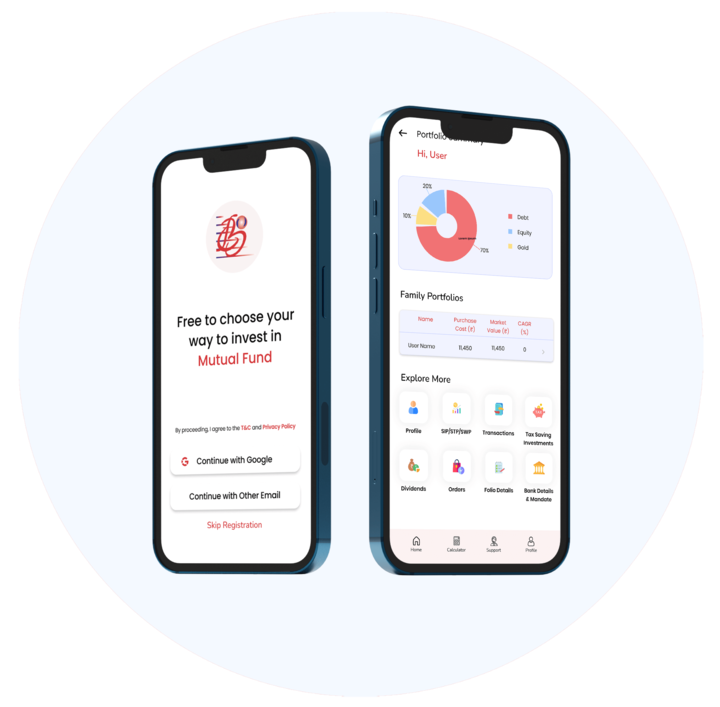

Prodigy Pro

A Quick, Simple & Paperless Investing Experience

The quickest and safest way to invest in Mutual Funds.

Invest, manage and monitor your money from the comfort of your home.

Hit the icon below to download.Know More

Join the BFC community to learn about investing, saving, and budgeting in the easiest ways possible! Whether you're a seasoned investor or just figuring out your financial journey, dive in for treasured insights and expert advice. Get tips on mutual funds, saving, budgeting, and retirement planning. Take control of your financial future today!

Invest smart! Give your investments the BFC Advantage

Tailormade Solutions

Tailormade Solutions Algorithm-based Scheme Selection

Algorithm-based Scheme Selection  Competent Wealth Managers

Competent Wealth Managers  Regular Profit Booking

Regular Profit Booking  App with 3 S Benefits

App with 3 S Benefits Capital Gain Immunization

Capital Gain Immunization  Tactical Calls

Tactical Calls

Signing up is quick and easy as 1,2,3.

Scheme recommendations based on investor priorities and superior Al logic.

A quick and straight- forward investment process.

Monitor your entire family's investments on one platform.

Biannual portfolio reviews to fish out bad investments.

The quickest and safest way to invest in Mutual Funds.

Invest, manage and monitor your money from the comfort of your home.

An honest attempt to educate investors on the Dos and Don'ts of investing.

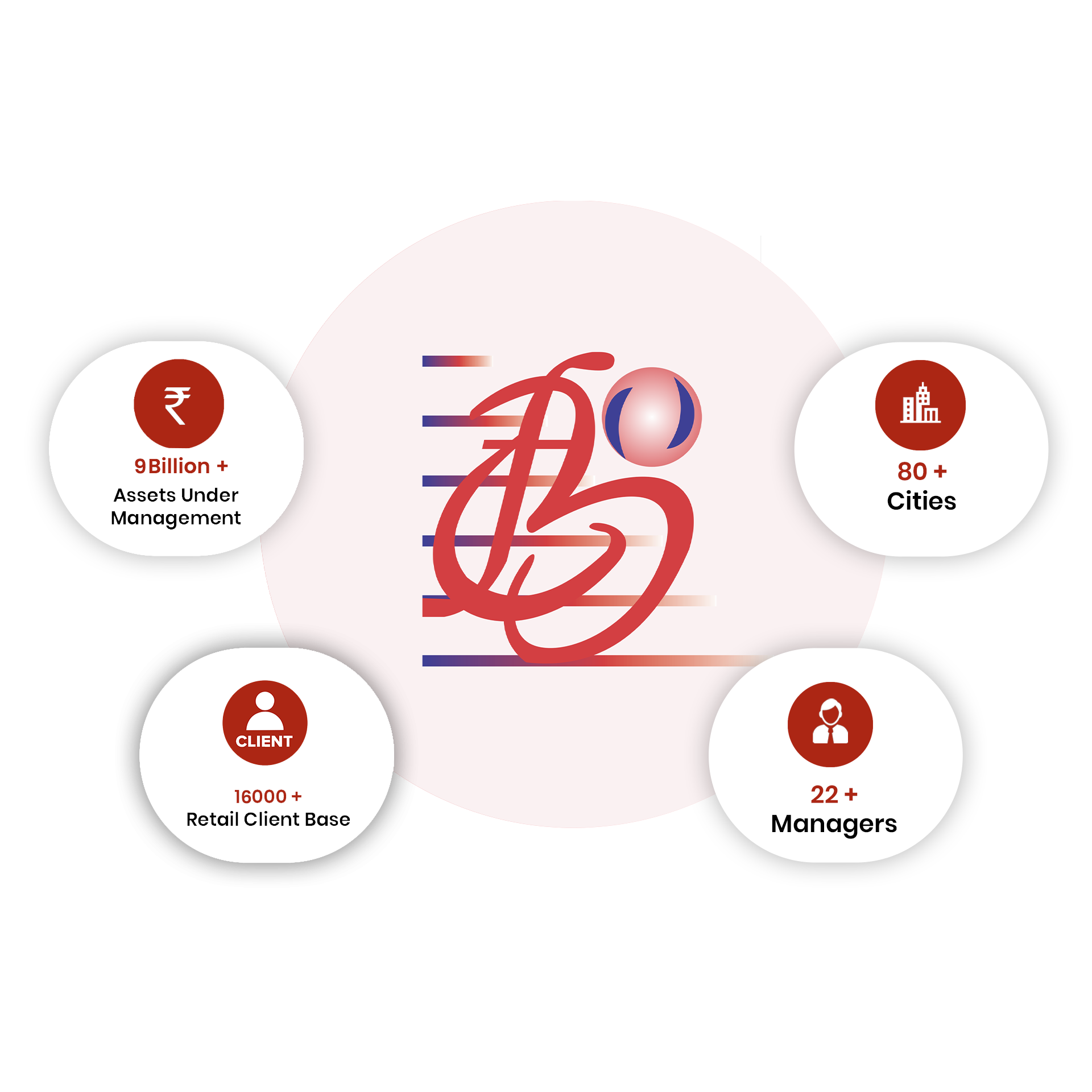

We haven't come this far to only come this far

Assets Under Management

Cities

Assets in PMS

Institutional Client Base

Retail Client Base

Managers

ARN : 21399, Date of initial Registration : 31-July-2004, Current validity of ARN : 29-July-2026

No : 39180

No : MFS21399

Here’s what our clients have to say about us

![]() I am delighted with BFC Capital’s services. It is refreshing to be associated with a company that keeps its client’s needs, and priorities ahead of other things. What impressed me was the way my Wealth Manager took care of my finances. She also provides regular updates and is available to answer any queries I have. I am particularly pleased with the advice offered on retirement planning, wherein a fixed income route was recommended. Transitioning into retirement will be much easier, thanks to the guidance offered.

I am delighted with BFC Capital’s services. It is refreshing to be associated with a company that keeps its client’s needs, and priorities ahead of other things. What impressed me was the way my Wealth Manager took care of my finances. She also provides regular updates and is available to answer any queries I have. I am particularly pleased with the advice offered on retirement planning, wherein a fixed income route was recommended. Transitioning into retirement will be much easier, thanks to the guidance offered.![]()

Mr. Anand Murti Srivastava

Mr. Anand Murti Srivastava![]() I have been a client of BFC Capital since 2011. Before this, I was into equity trading and faced huge losses due to the lack of proper advice. Also, I did not have any specific goal for investing. There were times when my portfolio was churned just for brokerage. At BFC Capital, my Wealth Manager understood my needs and guided me to invest as per my goals. My portfolio was structured keeping my interests in mind and therefore blossomed well.

I have been a client of BFC Capital since 2011. Before this, I was into equity trading and faced huge losses due to the lack of proper advice. Also, I did not have any specific goal for investing. There were times when my portfolio was churned just for brokerage. At BFC Capital, my Wealth Manager understood my needs and guided me to invest as per my goals. My portfolio was structured keeping my interests in mind and therefore blossomed well. ![]()

Mr. Virendra Chandra Singhal

Mr. Virendra Chandra Singhal ![]() BFC Capital has been my financial advisor for more than 2 years, and throughout this tenure, they have maintained great market awareness. What impressed me is the way my Wealth Manager streamlined the planning process to customize a financial plan that suited my profile and needs.

BFC Capital has been my financial advisor for more than 2 years, and throughout this tenure, they have maintained great market awareness. What impressed me is the way my Wealth Manager streamlined the planning process to customize a financial plan that suited my profile and needs.

She monitors my investments around the year and suggests necessary changes, if and when needed, for my benefit.![]()

Dr. Neerja Singh

Dr. Neerja Singh From first-time investors to seasoned clients, our community shares how BFC Capital made their investment journey smooth, secure, and success-driven.

Money matters are serious business.

Don’t take them lightly. Reach out to our

experts and make informed financial decisions.

+91-7347700888

+91-7347700888 customersupport@bfccapital.com

customersupport@bfccapital.com