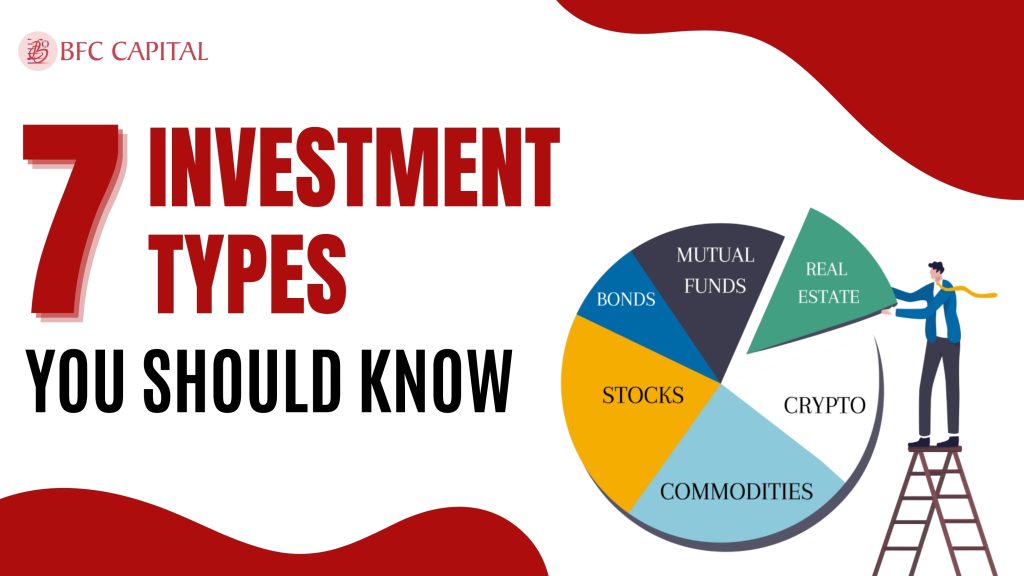

Types of Investments

Investing is one of the most important avenues of growing wealth through time, and that gives plenty of choices to individuals willing to hedge some of their choices against their financial future. Investors, either seasoned or beginner, should know what types of investments are out there and the peculiar advantages, risks, or returns each could have. This guide ranks seven mainstream types of investments and explains them in simple terms with relatable examples.

7 Common Types of Investments

There are different types of investments like stocks, bonds, mutual funds, and real estate—each with unique risks and returns to match your goals.

1. Stocks

Now, let’s start with stocks: the most popular form of investment. Buying stock means buying part ownership in the company. Think of it like buying a small piece of a big pie. When the company does well, your stock price goes up, and you can sell it for a profit. When the company does not do well, your stock price reflects that and goes down, so you might lose money.

For example, when 10 shares are purchased at ₹1,000 each, the long-term possibility exists that it may grow and the price may go up to ₹1,500 per share. Therefore, now selling them for ₹15,000 means you make a ₹5,000 profit. However, the company might be in a little bit of problem and the price of the stock has gone down to ₹500, and now selling will be a loss.

Stocks tend to be volatile, meaning their prices can change drastically very often. Hence, risk management through portfolio diversification would grow in importance in stock investing.

2. Bonds

For someone whose preference gravitates more to bonds rather than stocks because such means of investment are generally regarded as safer forms of investments, borrowing money from the government or business or even lending money, with the expectation of getting paid by them in interest and principal during a specified time frame. In addition to the inherent risk of failure, they are also considered less risky compared to stock investments, as well as offering more predictable returns.

Example: You buy a government-promised bond for ₹10,000 at an interest rate of 5% a year. The government is now liable to pay you ₹500 every year long as the end of the bond (usually after 10 years). In the end, you get your ₹10,000 back. Bonds are best appreciated with high yields of annual income and can also be tailored in investment portfolios for better asset allocation.

3. Mutual Funds

A mutual fund is an investment vehicle which collects money from all kinds of investors and invests it in some combination of equities, bonds, or other assets. These allow you to diversify your investments without buying individual stocks or bonds. It is a professional fund manager who takes care of all selection and management of such investments for you.

Example: Assume you want to invest ₹50,000 and have not yet decided what stocks to choose from. If you choose to invest your amount in a mutual fund, your money can be spread over many different stocks, such as one sector being invested in technology, others in health, and energy, so you will not lose all your money when one sector performs poorly. That last point is precisely why mutual funds are very appealing to those looking to invest and actively participate at the same time in multiple asset classes. They can also diversify portfolios and hedge against inflation since most tend to be less liquid than their related securities.

4. Real Estate

People invest in real estate by buying property, be it land, houses, or commercial retail space, expecting its value to appreciate over time. Real estate is less liquid than stocks but provides opportunities for passive income in the form of rent.

Passing off as an example: You buy an offshore property worth ₹50 lakhs in a growing area. On appreciation of property value over the years, you sell it for ₹70 lakhs, thus making a profit of ₹20 lakhs. However, rental of the property fetches monthly rental income.

5. Commodities

Investing in commodities means buying physical products, such as gold or silver or perhaps oil and agricultural products. High inflation usually implies that commodities would perform well and serve as an inflation hedge. Commodities can be purchased directly or through commodity-focused funds.

Illustration: If you buy gold worth ₹5 lakh and inflation inflates the price of gold, the investment goes up. Usually, prices of gold surge in uncertain economic situations, which means it is a good well for diversifying your portfolio.

These might be subject to high volatility prices in an international market and, in some cases, provide good tax-saving investments if held for a long period.

6. Fixed Deposits (FDS)

Fixed deposits have been one of the most peaceful kinds of investments for a long time. FDs refer to the deposit of a lump sum paid to the bank for a pre-agreed period (from a few months to a few years) wherein one earns interest. Interest on FDS is generally more than a savings account interest but less than what can be received on other forms of investments such as stocks and bonds.

Example: You put ₹1 lakh in an FD for 3 years at the rate of interest of 6% per annum. At the end of the tenure, you would receive ₹1 lakh along with ₹18,000 interest, totalling ₹1.18 lakh.

FDs are beneficial for conservative investors wanting guaranteed returns. A large portion of financial planning, especially for people who wish for short-term investments with guaranteed returns, revolves around such investments.

7. Recurring Deposits (RDS)

Recurring deposits (RD) are much like fixed deposits, except it is instead of a single, lump-sum amount, they want to deposit a fixed amount every month for a specific period. After the completion of the term, the principal amount plus interest is paid to the investor.

For example, you would invest ₹5000 each month in an RD for three years with an interest rate of 7%. At the end of the period, you will receive the interest earned, along with your ₹1.8 lakh investment. These deposits are pretty good for ones who cannot invest a huge lump sum but wish to invest slowly over a period of time.

Also, Check – Best Mutual Funds to Invest in 2025

Conclusion

To wind things up, investment is a good path to wealth creation and comes with many avenues with different objectives and risk appetites. From stocks, bonds, or mutual funds to real estate, commodities, fixed deposits, or recurring deposits, the need of the hour is to diversify the portfolio while understanding the risks attached to each form of investment. Capital appreciation, passive income, and tax-saving investments would remain your attention areas, but your financial objectives would make all the difference in providing the right choice.

Please share your thoughts on this post by leaving a reply in the comments section. Contact us via phone, WhatsApp, or email to learn more about mutual funds, or visit our website. Alternatively, you can download the Prodigy Pro app to start investing today!

Disclaimer – This article is for educational purposes only and does not intend to substitute expert guidance. Mutual fund investments are subject to market risks. Please read the scheme-related document carefully before investing.