Do you want good returns that also can save taxes but are unsure which investment plan is suitable for you? Both ULIPs and ELSS have their individual advantages, but which one will suit you is the question! Let us compare and contrast ULIPs and ELSS in this article to assist you in making an informed decision.

Understanding ULIPs

ULIPs are insurance products that combine the elements of insurance, investment and savings and this makes it distinct from other related products. They offer you life coverage – something that is akin to mutual funds where you are free to invest in either equity, debt, or both.

How do ULIPs Work?

An Ulip means Uniform Linked Insurance Plan or Unit Linked Insurance Plan, and it provides life coverage along with investment. At this point, when you obtain a ULIP from a life insurance company, the several amounts you make are called ‘premiums. ’ Few portions of these premiums are directed to the life insurance segment, and the rest get invested into particular funds like equity, debt, or hybrid options.

For example, An investor invested ₹10,00,000 on April 1, 2019.

Performance:

- Investment Horizon: 5 years

- Return: 11.21%

- Investment Value: ₹17,01,058.32

- Gain: ₹7,01,058.32

Analysis:

This example demonstrates the potential returns that ULIPs can offer. By investing ₹10 lakhs in ULIPs, the investor has earned a significant profit of ₹7,01,058.32 over 5 years.

Advantages of ULIPs

- Life Coverage: ULIPs offer an insurance part that gives adequate monetary security to your family in the consumer’s demise.

- Wealth Creation: The investment part of ULIPs has long-term income-generating capacity which in turn empowers you to meet your financial objectives.

- Tax Benefits: ULIPs provide an exemption from taxes on the maturity amount under section 10(10) D and tax relief on the premium paid under section 80C.

- Flexibility: By allowing you to switch between different funds, ULIPs help in chasing the market as well as risk appetite.

- Loyalty Benefits: ULIPs facilitate loyalty addition where the investor has to remain invested for the entire policy period. The payment of this bonus is according to the policy terms and conditions a bonus to policyholders who have maintained their policy.

Understanding ELSS Funds

Another benefit that can be discussed is that it can be viewed as a tool aimed at saving taxes. ELSS stands for Equity Linked Savings Scheme which is a Mutual fund scheme that has its leaning towards equity and is an instrument classified under tax-saving schemes. In the same way, Equity Linked Savings Scheme (ELSS) funds primarily invest in equities and equity-related instruments.. These funds primarily have the objective of achieving the highest possible return on invested wealth by deeply researching the market and then investing in stocks.

For example, An investor made an initial investment of ₹1,50,000 in an ELSS fund on April 1, 2017.

Lock-in Period Performance:

- Lock-in Period : 3 Years (01-04-2017 to 01-04-2020)

- Return: ₹4,457 (0.98% CAGR)

While the short-term return might seem modest, it’s important to consider the tax benefits and the potential for long-term growth.

Long-Term Performance:

- Investment Horizon: 7 Years (01-04-2017 to 04-09-2024)

- Return: ₹3,77,082 (18.44% CAGR)

As the investment horizon increased, the returns grew significantly. This demonstrates the power of compounding and the importance of staying invested for the long term.

The working of ELSS funds

ELSS funds can be broadly described as diversified equity mutual funds that predominantly seek to invest in equity asset classes. These funds invested in equities in firms that are floated in the stock market and categorically, these firms can be categorized along the market capitalization or size as well as along the industry in which they operate. Investing in ELSS funds aims to generate good returns through equity investments while allowing investors to claim tax deductions under Section 80C of the Income Tax Act. Long-term capital appreciation and tax benefits are the main goals of the investment, not high expenses.Portfolio managers similarly purchase the securities through research with the purpose of finding the best investment that has the potential of generating good returns with little risks.

Through ELSS funds, investors can get tax exemptions from the government based on the Investment under section 80C of the IT Act 1961. However, they are free to invest any amount of money they want, but the tax deduction is capped at Rs. 1.5 lakh.

Advantages of ELSS Funds

- Tax Savings: ELSS funds provide investors with tax benefits up to Rs. 1. 5 lakhs to your tax-exempt limit under section 80c of the Income Tax Act, thus effectively reducing your taxable income.

- Shorter Lock-in Period: ELSS funds also come with a three-year lock-in period, which is even more liquid and gives the option to withdraw the invested quantity after 3 years

Understanding ULIP vs ELSS with Example

Now, let’s consider ULIP as the train journey and ELSS as the flight that takes you to the same destination but with various features. ULIP is like the train since it provides insurance and also a journey to invest. This one takes a little bit more time (5-year lock-in) but gives full immersion. ELSS, however, is like the flight: nothing but investment takes you closer to your goal faster (with a lock-in period of 3 years) but does not have the safety net of insurance. On the one hand, there are some benefits to both routes, but it really depends on whether someone is interested in the process of reaching their insurance goal or simply just to meet their investment goals as soon as possible.

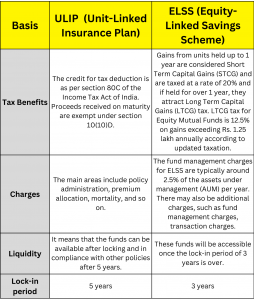

Difference Between ULIP and ELSS

Bottom Line

ULIPs and ELSS have their distinct features that help meet the needs of various investors. ULIPs offer both protection and savings/ investment, which makes it appropriate for those who want to get the two benefits from one product. However, given that ULIPs lock-in options are longer than mutual funds and the charges relatively higher, they make sense only for people with a long-term view and who require the additional life cover. On the other hand, ELSS is a purely investment-oriented tool that has comparatively less duration of lock-in period and has better chances of giving better returns due to the equity base. It is better suited for investors looking for tax benefits, flexibility, and the potential to achieve higher returns without requiring insurance coverage. Therefore, before investing in either of the two investment products, you need to understand your financial objectives, risk appetite, and whether one requires insurance coverage or not.

Please share your thoughts on this post by leaving a reply in the comments section.

Also, check out our recent post on: “What is the Sovereign Gold Bond Scheme (SGB)?“

To learn more about mutual funds, contact us via Phone, WhatsApp, Email, or visit our Website. Additionally, you can download the Prodigy Pro app to start investing today!

Disclaimer – This article is for educational purposes only and by no means intends to substitute expert guidance. Mutual fund investments are subject to market risks. Please read the scheme related document carefully before investing.