Macaulay’s duration is a fundamental idea that is useful in assessing how a bond is affected by changes in interest rates. In other words, it is the average time with a weight given to bonds of different maturities to receive their cash flows. It refers to the period that holding a bond neither loses the reinvestment risk nor is exposed to the price risk.

The concept of Macaulay Duration is highly relevant when deciding on purchasing a debt instrument. It can significantly assist investors in selecting between numerous groups of possible fixed-income securities within the market environment. Everyone knows that bonds are affected by interest rates and with that in mind let me continue. It aids investors in terms of which bond to buy, long term or short term depending on the duration the various coupon bonds are offering accompanied by the expected interest rate structure.

Calculation

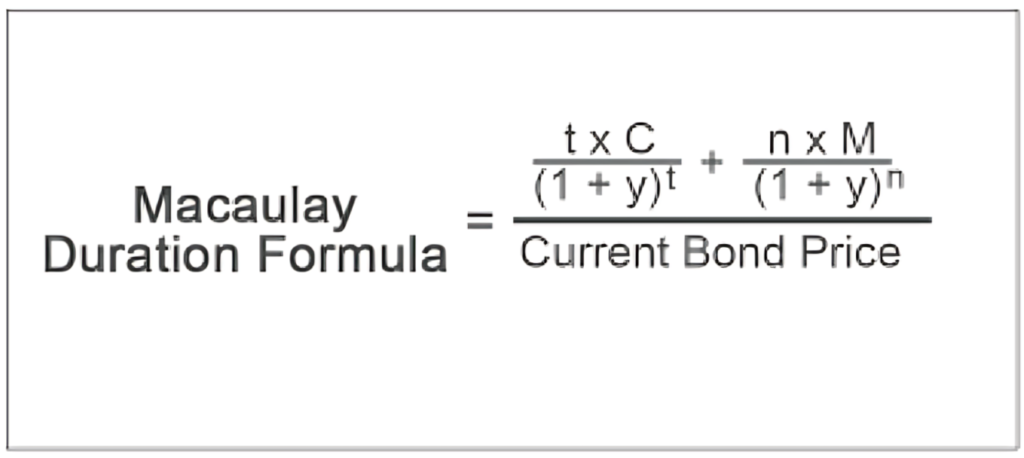

Macaulay Duration is calculated by using the bond’s cash flows with each cash flow being weighted by the proportion of that cash flow’s value in the total value of the bond at present.

Formula

Where,

t = period

C = coupon payment

y = yield

n = number of periods

M = maturity

Current Bond Price = present value of cash flows

Understanding with Example

Picture a seesaw in a children’s playground where now instead of two children, you have weights that are equal to the bond’s cash flows. These weights are placed at different time points indicating the time when such cash flows are expected to be received. Some weights are closer to the vertical middle line, indicating cash flows to be received shortly whereas the other weights are further from the middle line, pointing to cash receipts to be paid at a later date.

Now, the objective of this seesaw is to determine the middle point between the two equal points. The point where the weights are equal is referred to as the Macaulay Duration. It means that it reflects how long it will take you to get all of the payments of your bond and then weighted by the size and timing of those payments.

For example, if you are holding a bond that has high cash flows in the beginning, these early cash flows will help to move the balance point nearer or contribute to the reduction of the duration. On the other hand, if most of the payment is due later, the balance point moves in the same direction increasing the duration.

Consequently, the Macaulay Duration allows one to get a single figure as to how long it would take to get the money back on all the payments with due regard to their amounts. This measure is important for the investor because it also shows how the bond will be affected by changes in interest rates. If the duration is long, then the bond is volatile to the interest rate changes; this is like having a seesaw with weights placed far away.

In the same way that using something to level the seesaw, the Macaulay duration provides traders with knowledge about the risk involved when it comes to the bond and especially its sensitivity to changes in interest rates.

Working of Macaulay Duration

This is how it works:

- Time of the Money: This shows when the company will be required to make payments for both interest and principal.

- Determination of the Present Value: Here, all cash flows are discounted to their present values using bond yield to maturity for that particular bond.

- Calculation of Weights: The weight of each flow is derived by taking the present value of each flow divided by total present value.

- Weighted Mean: Multiply each number with its weighted time and sum them up together.

This gives us Macaulay Duration which demonstrates how much a bond is affected by changes in interest rate.

Merits of Using Macaulay Duration

It is vital in assisting the investors to evaluate the risk in fixed-income securities, based on the period. Like in equities, where risk can be measured by standard deviation or by possessing a security beta factor to measure the volatility of stock prices, risk in fixed-income instruments is mainly gauged by Macaulay duration. Hence, it is crucial to comprehend and contrast the Macaulay duration of other securities since it may be useful in identifying potentially ideal choices for a fixed-income investment portfolio.

Setbacks of Using Macaulay Duration

Hence, while duration gives a reasonable measure of price changes for bonds that do not contain options or other long-term contracts, it is most effective for small movements in interest rates. Furthermore, when the movement in rates becomes greater, convexity or the shape of the bond price yield curve becomes more pronounced. Because the relation between the bond’s price and yield is convex unlike linear, techniques like duration may not be accurate. The difference between actual and estimated prices also grows with yields, which is due to the process referred to as the degree of convexity, related to the nature of the line on the graph of bond prices.

Factors Affecting Macaulay Duration

- Price: The current price of the bond affects its duration, whereby lower prices correspond to higher duration.

- Maturity: Macaulay Duration usually rises with increases in the bond’s time to maturity implying that Bonds with long time to maturity have higher durations.

- Coupon Rate: Higher coupon bonds have short durations because they provide cash to investors before long-term bonds do.

- Yield to Maturity: When yield to maturity rises, the bond’s duration falls, meaning that its prices will not be as affected by interest rate fluctuations.

- Sinking Fund: Holding of a sinking fund which implies that the bond is partially paid before the due date also reduces the bond’s term.

- Scheduled Prepayments: Furthermore, prepayments that are made before the time of maturity of the bond also shorten the duration.

- Call Provisions: There is evidence of shorter durations when bonds have call provisions that enable the issuer to redeem the bond before its maturity.

Bottom Line

Having a good understanding of Macaulay Duration is important for the assessment of the future return on investment on fixed-income securities. This idea becomes even more significant when dealing with hardworking and frugal investors who want to diversify their risks as much as possible to get the highest returns. Thus, comparison between various bond securities based on the duration effectively helps investors in achieving diversification and maintaining portfolio stability despite volatile interest rates. Furthermore, interest rate risk, specifically recognizing bond prices and their duration as well, plays a crucial role in every investment decision. This approach helps protect investors and make sure that they have attained their financial needs with minimal risks.

Please share your thoughts on this post by leaving a reply in the comments section. Also, check out our recent post on: “What Is a Top-Down Investing and Bottom-Up Investing Approach?“

To learn more about mutual funds, contact us via Phone, WhatsApp, Email, or visit our Website. Additionally, you can download the Prodigy Pro app to start investing today!

Disclaimer – This article is for educational purposes only and by no means intends to substitute expert guidance. Mutual fund investments are subject to market risks. Please read the scheme related document carefully before investing.

Name: Line of Credit vs. Loans: Understanding the Key Differences

says:[…] Please share your thoughts on this post by leaving a reply in the comments section. Also, check out our recent post on: “Macaulay Duration: Definition, Formula, Example, and How It Works“ […]