In a Systematic Investment Plan (SIP), you invest a fixed amount of deposit at regular intervals – monthly, quarterly, etc. The SIP deposit can be as little as Rs. 500, making it one of the most convenient methods of mutual fund investments. SIPs help you to be consistent and disciplined towards your financial objectives. You allow the standing instructions on the chosen investing platform to debit a fixed amount to be debited from your bank.

One of the significant advantages of SIP is Rupee Cost Averaging (RCA). RCA allows you to purchase more units when at a low cost and fewer units at a high cost by averaging out the cost of your funds over a specific period. A lot of factors play a huge in determining your investments, most of these such as debt or equity, are intricately linked. But while using SIP, you don’t have to worry about market conditions or time.

The common strategy used in investing is “purchasing low and selling high”. It reduces potential risks and offers you better returns on your investments. If you want to commit to long-term investment plans that don’t retain the risks of an equity market, SIP is a simple and viable approach for you. Once you regulate transactions along a fixed schedule, you can maximize your returns to a significant value.

What is the Rupee Cost Averaging (RCA) Strategy Used in SIP?

Imagine there are two different scenarios – the market rises and declines. Now, we will study the effectiveness of investing using the rupee cost averaging method using this example. It will illustrate how this method helps mitigate market risks in the long haul.

To successfully examine this example, we will make three significant assumptions:

- The monthly investment is Rs. 5,000.

- The investment period is 10 months.

- We are assessing two major market scenarios:

- Market rises: The NAV increases from Rs. 100 to Rs. 150 over 10 months.

- Market declines: The NAV decreases from Rs. 100 to Rs. 70 over 10 months.

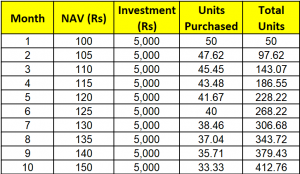

Scenario 1: When the Market Rises

=> Total value after 10 Months = 412.76 ✕ 150 = Rs. 61, 914

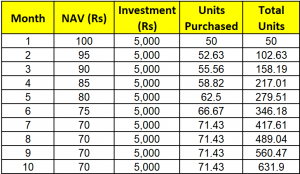

Scenario 2: When the Market Declines

=> Total value after 10 months = 631.90 ✕ 70 = Rs. 44,233

Analyzing the Scenarios: How Does Rupee Cost Averaging Work?

The Net Asset Value (NAV) increases from Rs. 100 to Rs. 150 in the first case where the market rises. During this period, you purchase fewer units every month. But, you also continue investing consistently.

Hence, you benefit from the lower prices during the initial months. Your total investment of Rs. 50,000 has increased to Rs. 61,914 reflecting a profit by the end of the investment period.

Alternatively, in the second scenario, you invest while the market declines. The NAV decreases from Rs. 100 to Rs. 70. However, in this case, you purchase more units as the price drops every month. This allows you to gather a large number of units for the same amount of investment i.e., Rs. 50,000. At the end of the investment period, your total number of units increased to 631.90 from the initial 50 units.

The second scenario illustrates that RCA can enhance future gains. As seen above, you end up with a lower average cost per unit by investing the same amount consistently. The more the market declines, the more units you acquire for your fixed investment. Hence, when the market rebounds, these units might offer you higher possible returns.

Learning Outcome: Merits of Using Rupee Cost Averaging Method for Mutual Fund Investments

Rupee Cost Averaging shows the merits of accumulating more units, as in the case of the second scenario. The more units you acquire, the better the chances are for potential gains when the market recovers.

Moreover, as given in the above example, the average cost per unit is lower in a SIP approach than in a lump-sum investment. This lowers the average cost leading to greater profits when the market recovers.

RCA’s strategy is averaging out the cost of your funds irrespective of the NAV. When the market declines, you control the overall cost. The average cost remains the same as the purchase cost. So, when you purchase more units with low NAV, the average cost drops.

Additionally, the investment plan follows a set calendar, so, you are the one who reduces the complexity of trying to balance the cost of your units with the effects of an unsteady market.

Concluding Points: Should You Invest in SIPs Using the Rupee Cost Averaging Method?

In a nutshell, Rupee Cost Averaging (RCA) reduces potential risks while attempting to time the market to align with your investment plans. It is quite difficult to predict how the market moves, but SIP through RCA negates the need to make such predictions.

The market remains as unpredictable as before. And, rupee cost averaging is gaining popularity among investors. RCA might not guarantee you profits but they lower the cost of acquisition over time to maximize returns in the long run. This approach is highly affordable and you can capitalize on market fluctuations while regularly investing for long-term income generation.

Start investing early to secure a stable financial future. Rupee Cost Averaging (RCA) remains one of the best approaches for beginners and eliminates any hassles or panic concerning the market.

Please share your thoughts on this post by leaving a reply in the comments section.

Also, check out our recent post on: “The Power of Mutual Funds: Building Wealth the Smart Way”

To learn more about mutual funds, contact us via Phone, WhatsApp, Email, or visit our Website. Additionally, you can download the Prodigy Pro app to start investing today!

Disclaimer – This article is for educational purposes only and by no means intends to substitute expert guidance. Mutual fund investments are subject to market risks. Please read the scheme-related document carefully before investing.

Name: What are Passive Mutual Funds: Meaning, Types, Risks, and More! - BFC Capital- Blogs : All Financial Solutions for Growing Your Wealth

says:[…] Also, check out our recent post on: “What is Rupee Cost Averaging in SIP & How Does it Work?“ […]